The Geography of Growth

A Fictional Tale of Two Fintech Success Stories

A fintech founder in Lagos stares at her screen, studying Stripe's $50 billion playbook. Meanwhile, her counterpart in San Francisco pores over M-Pesa's dominance in Kenya. Both search for answers in each other's success, yet both might be looking in the wrong direction. The path to a billion-dollar fintech isn't a straight line - it bends with the terrain it travels.

The notion that financial technology transcends geography is seductive but flawed. Money moves differently - whether in San Francisco, Lagos, London or Mumbai. But these differences aren't just about infrastructure or income levels, they’re heavily influenced by invisible architecture of trust, the rhythm of daily commerce, and the DNA of financial behavior. While San Francisco optimizes for convenience, Lagos solves for accessibility. Where one builds on existing digital infrastructure, the other must often create new pathways through informal networks.

The contrast becomes clear when we map the journey of fintech founders in both markets - their paths diverge not just in strategy, but in the very foundations of how they build value.

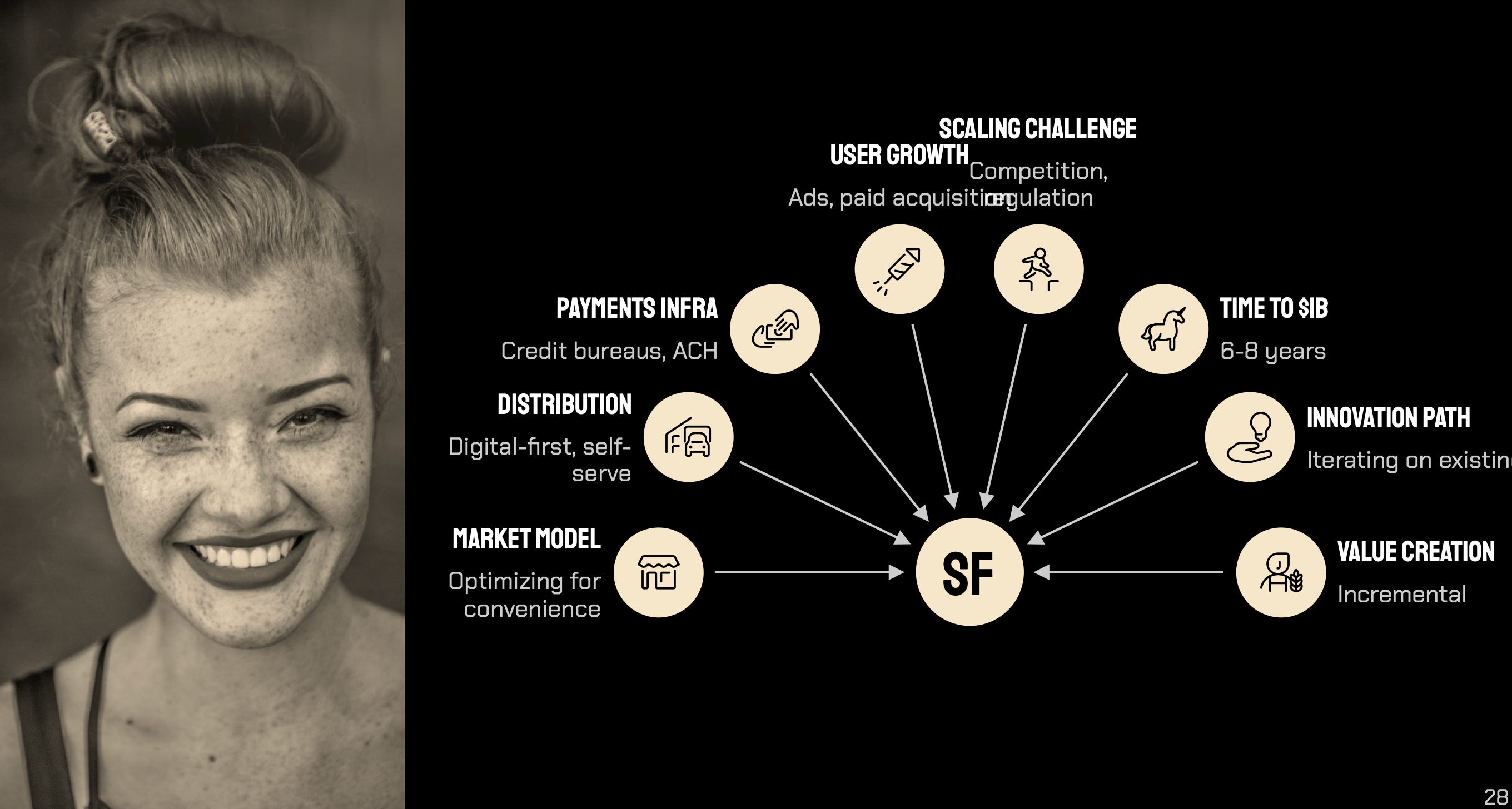

Consider trust. In San Francisco, it's institutionalized - encrypted in bank vaults and secured by regulatory frameworks. Credit bureaus and ACH systems form the bedrock of financial innovation. Stripe succeeded not by building trust from scratch, but by making trusted systems work better together. But cross the ocean to Lagos, and trust flows through different channels. Here, it's woven through community networks, embodied in local agents, and validated by word-of-mouth more than any security certification. Mobile money and cash economy dynamics shape the foundation of financial innovation.

This dichotomy shapes everything. While Stripe scales through elegant APIs and seamless integrations, companies like Moniepoint grow through networks of human nodes - agents who convert digital promises into physical cash, who turn corner shops into financial hubs. Their technology isn't just connecting systems; it's connecting communities.

The user growth stories tell a similar tale of divergence. San Francisco's path runs through ads and paid acquisition, fueled by venture capital willing to subsidize customer acquisition. Lagos builds differently - through word-of-mouth and community-led adoption, where trust travels through social networks rather than social media.

The innovation paths diverge just as sharply. Silicon Valley iterates on existing models, making good systems better. Lagos often leapfrogs entirely, creating new models where old ones never took root. One refines the present; the other reimagines what's possible.

The revenue streams tell a similar story of divergence. In developed markets, interchange fees flow like rivers, feeding ecosystems built on card swipes and digital transfers. But in cash-dominant economies, revenue must be carved from different stone - transaction fees, agent commissions, and the gradual building of alternative credit models that make sense of informal incomes.

Time itself moves differently across these markets. A monthly subscription model that hums smoothly in New York might stutter in Nairobi, where income arrives in daily waves rather than monthly tides. The same fintech solution, transplanted without translation, withers in foreign soil.

M-Pesa grasped this early. They didn't just launch a mobile money service; they built a new financial language that spoke to local realities. Their agents weren't just service points; they were trust translators, converting digital concepts into tangible value. This wasn't about technological superiority - it was about contextual fluency.

The implications ripple beyond product design into the very fabric of growth strategy. While Silicon Valley fintechs can burn venture capital to acquire users, betting on lifetime value, their emerging market counterparts must find sustainability earlier. The luxury of growth before profitability often doesn't exist where capital markets are thinner and user economics more fragile.

Yet this constraint breeds innovation. Unable to rely on pure digital scale, emerging market fintechs excel at hybrid models - part digital, part physical, fully embedded in the realities of their markets. They build not just apps but ecosystems, not just platforms but bridges between formal and informal economies.

The path to a billion dollars in fintech isn't universal - it's intimately local. Success doesn't come from copying global playbooks but from reading local signals. In developed markets, it might mean making the efficient more elegant. In emerging markets, it often means making the informal more accessible.

For founders and operators, the lesson isn't about choosing between these models but understanding which truths translate and which must be discovered anew. The future of fintech won't be written in one language but in many dialects, each speaking to its own market's unique rhythm and rules.

The most successful fintechs don't just move money - they move with the market they serve. They understand that while technology may be global, trust is local, behavior is cultural, and growth must be native to survive.

“Contextual fluency”. That’s a beautiful framing. *Adds to lexicon database*

As always, thanks for sharing your knowledge, Adia 👌🏾

Wow!

This piece really resonates with me. I recently wrote about the mistakes I’ve made while building a business in Nigeria, and it all comes back to one thing: context is everything.